2023 Annual Letter: The State of Venture

Here are the tectonic shifts we’re paying attention to in the tech market—and how our investing philosophy fits in.

Table of contents

Over the last 18 months, the contrast between bleak macro signals and growing optimism around technology breakthroughs has reached new heights.

Below, we share some of our observations about the world around us—and how they inform our approach to investing and portfolio management at M13.

Our venture philosophy

Sitting here in September 2023, we believe this is a tremendous time to be making venture capital investments.

Aversion to loss is a basic human condition. Athletes often say the pain of losing is greater than the joy of winning, and this is true in VC too, despite loss being a significant part of how this asset class performs (35% of investments typically go to zero). At M13, we understand that challenging macro conditions are not just unavoidable, but healthy: headwinds can provoke necessary resets and ultimately create a stronger ecosystem.

With capital tightening, company mortality will continue to rise, freeing up talent and dollars for new opportunities. Exceptional founders are not worried about rates (they will go down) and multiples (they will expand). And 2023, 2024, and 2025 will be tremendous years to make seed and Series A investments given the technological breakthroughs we are living through (more on these below).

Regardless of cycles, a few of our investing philosophies remain the same:

.png)

We need to invest in the exceptional.

It’s not enough for a founder to be smart or a company to be a minor improvement in a crowded space; we’re only interested in backing exceptional founders who are bringing true innovation to their market (or creating an entirely new one). We don’t get excited about incrementality.

.png)

The juice has to be worth the squeeze.

We seek the superlative outcomes that come from backing exceptional founders creating market leaders. We lose even when a company works but its scale and ambition aren’t big enough.

.png)

Great products ≠ great businesses.

It can be easy to fall in love with a great product as an end user, but an investor mindset requires thinking beyond the product to evaluate business models, capital intensity, delivery mode, cash management, and headwinds and tailwinds.

.png)

We believe in a wide path to great returns.

We respect the power law and believe the majority of our returns will be driven by a select number of investments. We also believe we can generate additional value through our active approach to portfolio management

How we got here: the macro landscape

While we are not macro economists, we do pay close attention to the public markets, key economic indicators, and important cultural shifts that shape our society.

Here are a few of the major macro and industry events that have taken place since the beginning of last year:

Rates go up: The Fed begins to raise interest rates to combat inflation, which peaked at 8% after over a decade of quantitative easing supercharged by a once-in-a-century global pandemic. As of today, interest rates have grown 525 bps since March 2022.

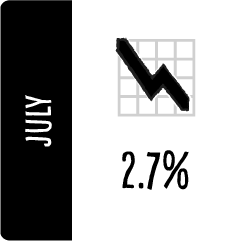

Savings go down: The consumer savings rate drops to 2.7%—the lowest level since 2005.

Musk buys: After months of waffling and legal back-and-forth, Elon Musk completes a $44B deal to purchase Twitter.

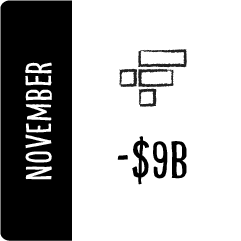

FTX falls apart: The failure of crypto platform FTX becomes one of the biggest VC-backed failures in modern history, losing some $9B of customer funds.

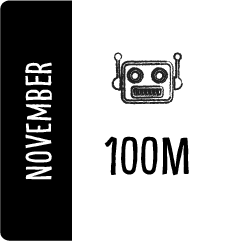

AI blows up: OpenAI launches generative AI tool ChatGPT and breaks the record for the fastest-growing app by reaching 100M users in less than 2 months.

TSwift tours: Taylor Swift begins her record-breaking Eras Tour, which is projected to gross more than $2.2B.

Banks crumble: Four major bank failures rock the tech industry: Silicon Valley Bank, Signature Bank, First Republic Bank, and Heartland Tri-State Bank, upending nearly $570B AUM.

Venture slumps: Quarterly global venture funding reaches a new 12-quarter low, hitting its lowest levels since Q2’20.

Apple resurfaces: Apple announces its spatial-computing-based Apple Vision Pro headset—the company’s first major product announcement in 9 years, since announcing the Apple Watch in 2014.

Messi scores: World Cup winner Lionel Messi moves to MLS, and in a first-of-its-kind contract will receive a revenue share of subscriptions to MLS Season Pass on Apple TV+.

Looking back, while we couldn't predict some of these events—particularly these cultural movements—the overall market correction is something we predicted a while ago. Our 2019 letter to investors acknowledged that the historically long bull market of the 2010s would not last. We were a few years early, but ultimately, the correction arrived.

But today’s conditions are no more everlasting than yesterday’s. Core inflation is back under 4%. Although travel and experiences remain expensive, air travel has returned to pre-pandemic levels, and in March, Las Vegas reached a new monthly high for visitors. It turns out human desire for connection and experience is unshakeable, and the rebound from years of staying put and staying apart has been strong (just look at how hard it is to get Eras Tour tickets).

Beyond the Fed, one of our biggest combatants to inflation is AI productivity. In coming months, innovations in this space should drive down costs and make things cheaper. Developers using AI coding assistants code 50% faster, while AI designers cost about a penny to create images that would cost $150 in human labor.

These tools are poised to lead to a generation of new outlier companies and great VC returns—reminding us all yet again that tougher days ultimately create the most enduring businesses.

The tech layoffs of the last year also mark a major shift in the workforce: a huge number of experienced operators are now on the job market. Equipped with ever-expanding AI productivity tools, these workers represent a new class of potential entrepreneurs—and investors should be paying attention to the potent tech and talent combination happening in this moment.

Where M13 invests and why

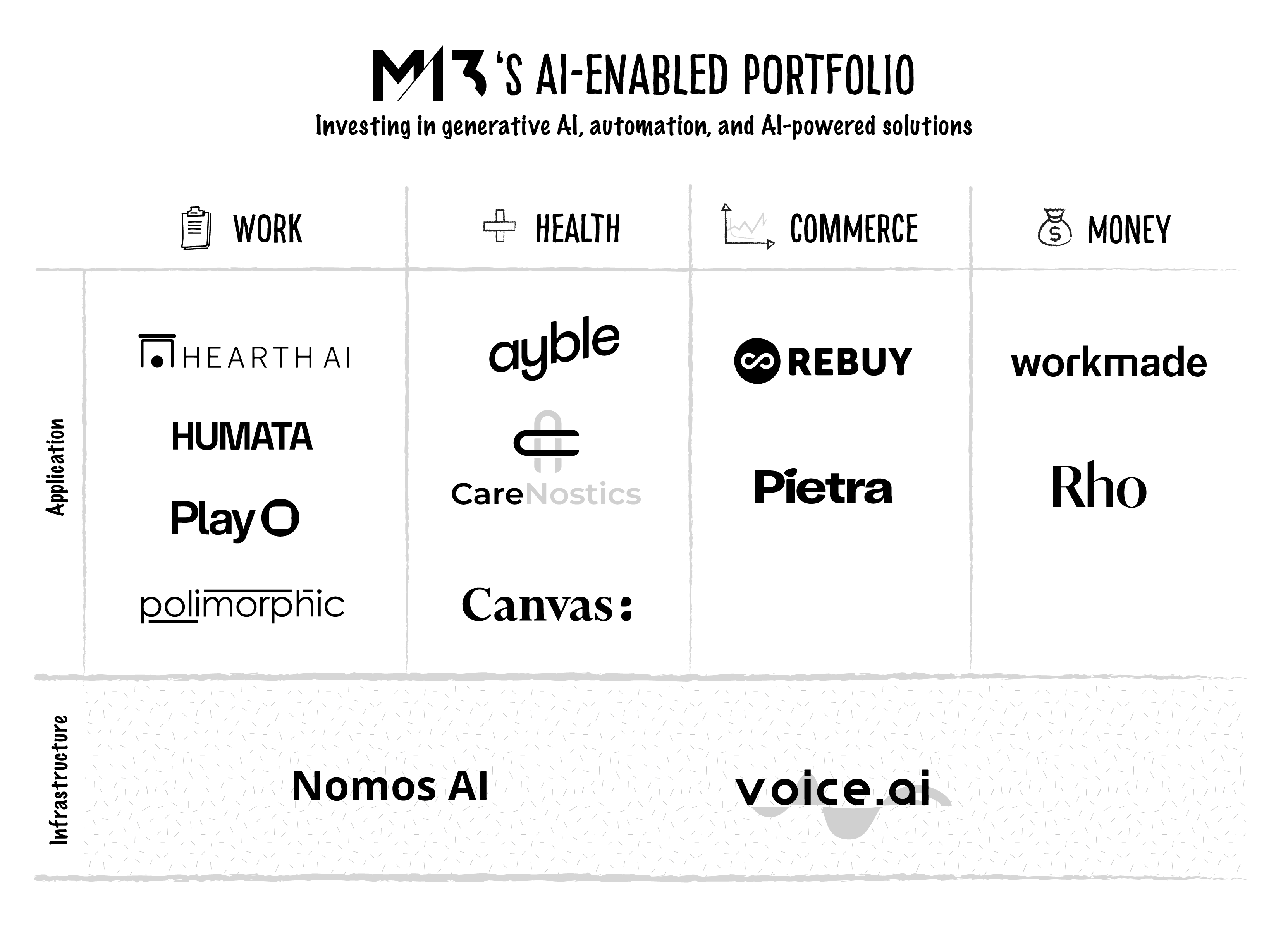

At M13, we invest in technologies shaping the future of work, health, commerce, and money.

While our heritage is in consumer technologies (2015 vintage investments include Lyft, Ring, ClassPass, Daily Harvest, and Rothy’s), we shed that label long ago. Over the last two years, more than half our investments have B2B business models. As customer acquisition for B2C companies has become more challenging, we’ve moved deeper into the tech stack to focus on enabling technologies selling to businesses.

In e-commerce infrastructure, we have invested in Pietra, Rebuy, and Max Retail, all of which service brands (not end users). Some of our fastest-growing fintech investments have been in companies like Rho and Ampla, which serve the middle market and CPG companies, respectively. Canvas Medical is focused on the intersection of clinicians and developers.

We are also excited about new companies in a theme we are calling “consumerization of government.” Upwards offers child care benefits to Fortune 500s and government employers, benefiting from the tailwinds of government childcare subsidies; Prepared brings a connected multimedia solution in public safety, targeting municipalities and corporations; and Polimorphic is building the first Constituent Relationship Management (CRM) software for local governments.

Our belief is that M13 portfolio companies can expand markets. We are constantly looking for the early tailwinds that will propel our founders forward. We invested in bitcoin infrastructure company Lightning Labs (2019) long before the Lightning Network was discussed on CNBC, and in telehealth weight management clinic FORM (2021) well before Ozempic was common dinner table conversation. We invested in local meal delivery platform Shef (2019) and the aforementioned Upwards (2022) based on regulatory and cultural tailwinds that have accelerated those businesses and given them the chance to be market leaders.

We’re compelled by the tailwinds created by frontier technologies like AI and blockchain—and we get especially excited about how they intersect within our vertical focus areas. We’ve already invested in several AI-powered solutions and actively seek out opportunities to back the next generation of founders building with this transformational technology.

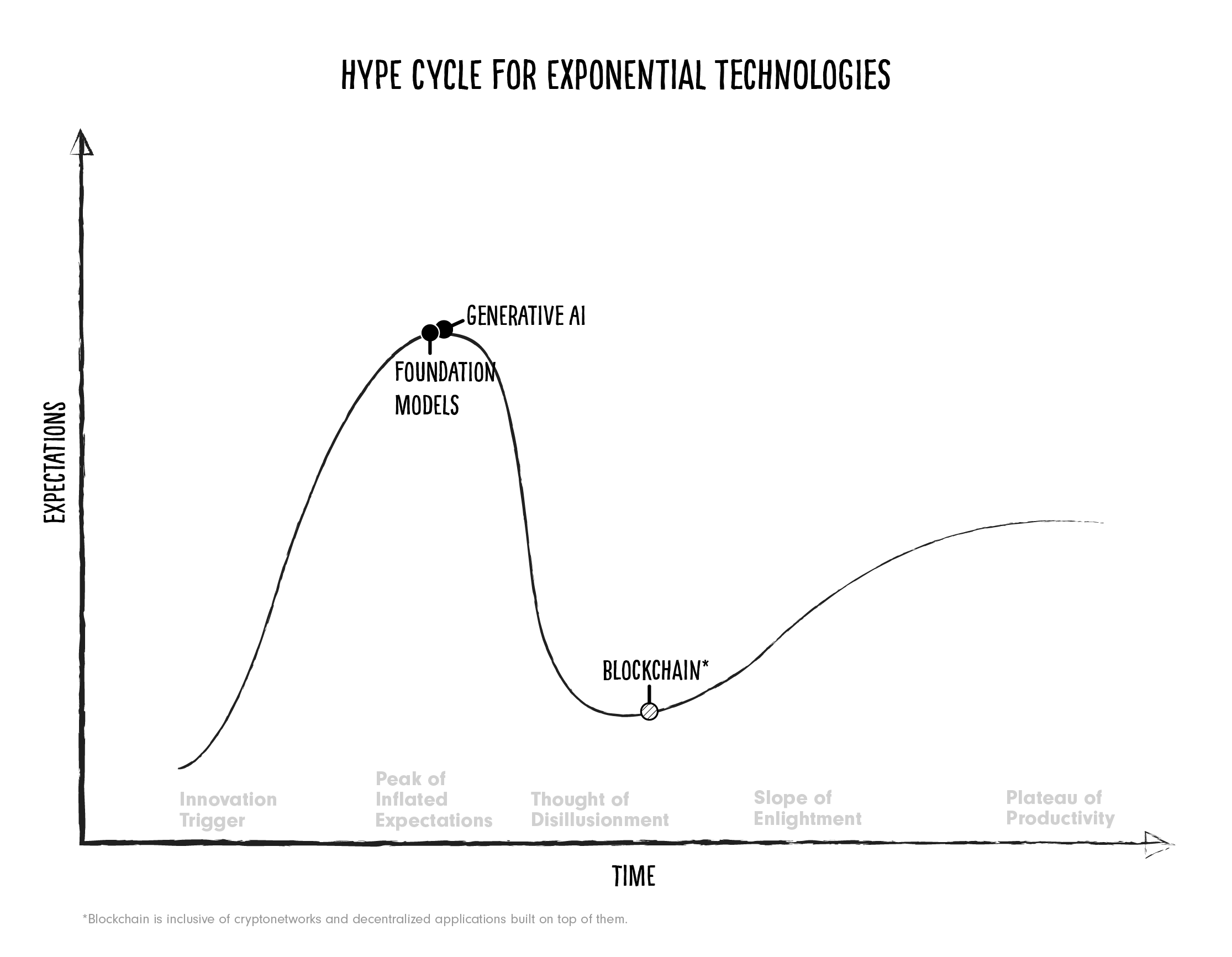

The exponential power of horizontal technologies

We agree with macro investor Raoul Pal when he calls this moment “the exponential age,” a new era defined by transformative technologies that drive exponential progress. AI and blockchain are well on their journeys through the hype cycle, and these powerful underlying technologies are playing a significant role in our portfolio and approach to investing.

Inspired by Gartner's hype cycle.

We believe both present very compelling areas to invest—although we are mindful of where each of these technologies sits in its respective hype cycle and of the mania and valuation creep that comes with the top of any hype cycle.

Artificial intelligence

As investors in AI, we focus on vertical applications with clear use cases and strong data advantages, as well as critical infrastructure platforms to support the growing application layer.

In the long run, we are preparing for a future where agent automation is possible, and AI can autonomously execute more complex multi-task processes.

In addition to exploring the impact AI is having on productivity, we are also looking for companies focused on prediction and provenance.

Prediction — Today, AI is already used in causal and predictive models to forecast the future. Combined with the power of generative features, we believe this power will become embedded in everyday workflows and products. In finance, AI will enable automated alternative underwriting and fraud response. In healthcare, traditional ML models can be used in conjunction with new generative features to facilitate early disease detection (see our company Carenostics) and treatment pathways—for example, notifying physicians of early signs of sepsis vs. the common cold and prompting treatment plans.

Provenance — What will generative AI mean for artists and creators? While Nick Cave may think the ChatGPT’s interpretation of his catalog “sucks," Holly+ embraces the possibilities of generative AI for artists, and singer Grimes is allowing musicians to leverage her likeness (“GrimesAI voiceprint") in exchange for a royalty split pending her approval. There will also be questions around high-fidelity, unauthorized content, and IP holders will have to decide: will they help distribute these projects to capitalize on them, will they ignore them, or will they try to end them?

We’ve seen the impact of AI across our portfolio, from companies explicitly creating AI products, to those that leverage it to power other offerings, to those using AI tools to improve their own operations:

- Canvas is using AI to help doctors scale up high-quality care and avoid insurance headaches

- Carenostics leverages AI to pinpoint individuals at risk for chronic diseases, empowering medical practitioners to make more accurate and timely diagnoses

- Hearth AI envisions agentic network management as the next generation of the CRM, centralizing, enriching, and prompting recommendations and actions across users’ personal networks

- Play auto-generates code as users design mobile-optimized applications

- Polimorphic offers software that automates constituent services for local US governments

- Rebuy is a commerce AI company that provides intelligent recommendations and personalized shopping experiences for consumer brands

- Rho is offering AI-powered invoice and bill processing to clients, using AI to digitize invoices

Blockchain

We haven't forgotten about crypto, web3, and blockchain. The immutable records of blockchain may be used to differentiate between AI and human expression, and concepts of governance, ownership, and tokenization which will be critical as we think about copyright.

The need for trustless, decentralized technologies is clear. Stablecoins and digital money are a massive use case—with a global stablecoin market cap size of $124 billion—and have clear product-market fit in emerging markets. Pakistani retailers use stablecoins to hedge against fluctuations in the rupee, something common across developing economies. Beyond emerging markets, Solana’s integration with Shopify allows businesses to make payments with stablecoins for fractions of a penny.

The themes of decentralization and open protocols will be even more vital as blockchain and AI begin to intersect. Our company Lightning Labs has recently enabled AI to send, hold and receive Bitcoin, which will help AI exchange value in a single denomination at a global scale.

We’re also interested in bringing real-world assets on chain. For example, M13 company Nori's carbon credits marketplace fixes significant accounting and transparency issues that have plagued the carbon market.

And let’s not forget: crypto is one of the best performing asset classes of 2023, with Bitcoin market cap growing 57% YTD. BlackRock CEO and previous crypto skeptic Larry Fink has called Bitcoin an “international asset,” arguing digital asset technology could “revolutionize finance.”

Questions remain. Can crypto expand beyond financial use cases? When and how will it intersect with AI? Fred Wilson’s post on the freedom to innovate is a great call to arms.

The road ahead

At M13, we are spending the time to understand the specifics of these fast-moving technologies as well as taking steps to be sensitive to their market timings and positions in the hype cycle.

Ultimately, we measure ourselves by the impact our portfolio companies have on the world around us, which drives distributions to our limited partners. The tectonic shifts taking place in technology and talent right now indicate this is indeed a golden time to invest and drive significant impact for years to come.

We are actively investing in the current market. Read about some of our latest investments here.

If you are a founder and the themes in this letter resonate with you, please reach out to latif@m13.co.

The views expressed here are those of the individual M13 personnel quoted and are not the views of M13 Holdings Company, LLC (“M13”) or its affiliates. This content is for general informational purposes only and does not and is not intended to constitute legal, business, investment, tax or other advice. You should consult your own advisers as to those matters and should not act or refrain from acting on the basis of this content. This content is not directed to any investors or potential investors, is not an offer or solicitation and may not be used or relied upon in connection with any offer or solicitation with respect to any current or future M13 investment partnership. Past performance is not indicative of future results. Unless otherwise noted, this content is intended to be current only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in funds managed by M13, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by M13 is available at m13.co/portfolio.

At a glance

There are no Cinderella stories. Blockbuster venture successes are always preceded by years of sleepless nights.”

There are no Cinderella stories. Blockbuster venture successes are always preceded by years of sleepless nights.”

—Sarah Tomolonius, M13 Partner & Head of Investor Relations

Further reading

.webp)

.webp)

© 2026 M13. All rights reserved.