Investing in the Future of Health: Digital Health for Specialty Care

Digital solutions are seizing the opportunity to lower costs and improve outcomes in some of the most challenging and common underlying chronic conditions.

Table of contents

This is the latest article that takes a closer look at M13’s Future of Health thesis.

Chronic diseases are the leading driver in US healthcare expenditure, making up approximately half of US healthcare spent or 10% of GDP. These conditions are generally ongoing and cause functional restriction, but can oftentimes be prevented. Managing a chronic illness is a lifelong and complex task that includes medication regimes, regular doctor visits, and surgical procedures. This burden of chronic diseases often shatters productive lives with fragmented patient journeys and expensive medical bills. However, we know that this burden can be lessened with early detection, lifestyle changes, medication management, and therapy. Digital health has great potential to deliver these integrated services and greatly improve chronic care management.

M13 has been investing in and studying digital health specialty solutions. These companies incorporate high-touch continuous interaction and digital care models that have the potential to simultaneously decrease the total cost of care and improve patient outcomes and quality of life.

In this article, we will share:

The magnitude of chronic disease and their impact on overall healthcare costs

Five areas of chronic conditions make up a significant part of the $4.1T annual healthcare spend in the US: musculoskeletal (MSK), heart diseases, neurological conditions, gastrointestinal conditions, and diabetes. This is not an exhaustive list of all chronic care but they are among the most prevalent. Chronic conditions often occur simultaneously, and addressing the underlying causes could have positive implications for multiple diseases.

The following diagram details the number of Americans struggling with common chronic diseases. We believe there is a potential for digital health solutions to intervene, especially when it comes to protocol adherence and early detection and intervention. The promise of digital health is reducing disease severity and ultimately the number of people impacted by these chronic conditions.

Another promise of digital health is that its accessible and prevention-focused care models can reduce unnecessary medical costs. While research detailing expenditures by condition varies, we have noted our sources and do not expect that digital health solutions will fully replace the need for all direct medical costs. Direct medical costs—from doctor's visits and medication to hospitalization and surgery—tell only part of the chronic condition story: disability and loss of productivity are some of the indirect costs that drain billions from our health system annually.

Market maps: companies and chronic conditions

Below are the five featured chronic conditions and ways that digital care companies are working to achieve better patient outcomes and lower cost of care.

Cardiovascular conditions: shifting acute to preventive care

In most cases, a good cardiologist can achieve great patient outcomes and address hypertension by coaching their patients on lifestyle changes and properly adjusting their medication plan. However, this requires a lot of high-touch interactions and time that many doctors often don’t have.

Virtual-first care enables these high-touch journeys with more efficiency and greater convenience for patients. They also have the opportunity to improve access to cardiology care and increase rehabilitation completion rates. For example, cardiac rehab is proven to reduce hospital readmissions by 50%, but 90% of patients do not participate in these programs because they lack access or have no convenient option to enroll.

Virtual cardiac recovery-focused businesses like Recora, Carda Health, and Moving Analytics partner with providers to offer everything from live exercise, nutrition, and mindfulness at the touch of a button. Virtual first cardiology providers like Heartbeat Health, Gordy Health, and Ventricle Health are more focused on prevention and offer full-stack clinical services including in-home diagnostics.

Gastrointestinal (GI) conditions: personalizing treatments

GI conditions like Inflammatory Bowel Syndrome (IBS) and Inflammatory Bowel Disease (IBD) are chronic and will require a lifetime of disease management. There is little known about prevention, so most solutions are focused on offering high-touch and iterative treatment plans. Tracking symptoms and behaviors like diet, sleep, and psychological conditions can help identify personalized triggers. Understanding these triggers can inform treatments that result in reduced symptoms and less frequent, less severe flares.

In combination with in-person visits, digital care programs and complementary care providers are able to deliver personalized treatments at scale. For example, Agora Health has developed a clinically validated personalized elimination diet program proven to drive significant remission rates among IBS and IBD patients. Agora works with patients, providers, and care coordination partners to bridge necessary gaps between in-person visits. Oshi and Vivante are partnering with employers to offer diagnosis and care management as an employee benefit.

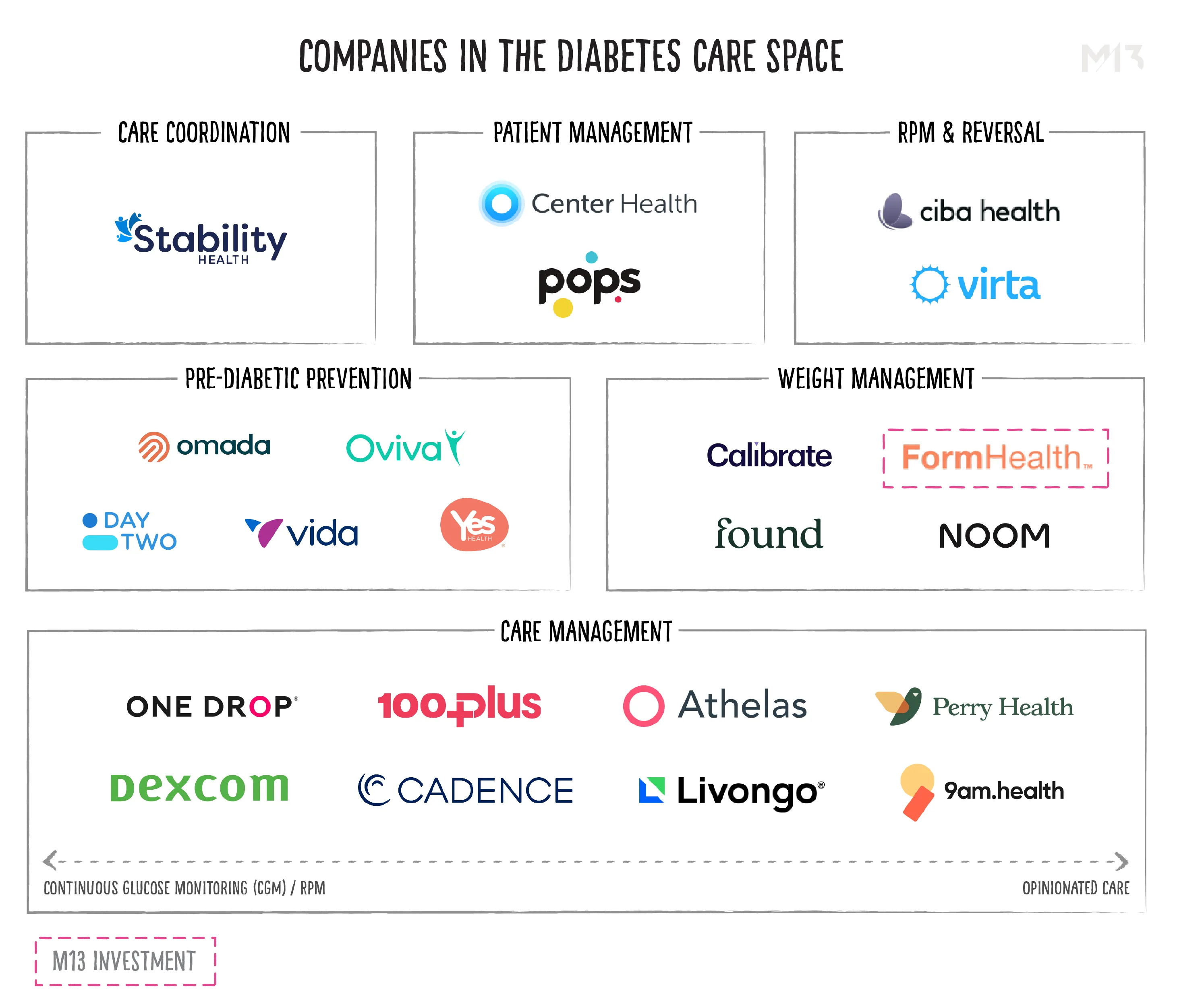

Diabetes / pre-diabetes: real-time monitoring and care guidance

Diabetes patients can live a very normal life with proper measures including weight management, lifestyle changes, and the right prescription drugs. If not managed, diabetes can result in severe (and costly) consequences such as eyesight, kidney, and nerve damage; high blood pressure and cholesterol that increases the risk of stroke; and infection and sores that require amputation.

Continuous monitoring solutions are becoming more pervasive. Monitoring solutions help patients and doctors continuously track how well this condition is managed and whether progress is being made. Companies focused on providing real-time monitoring and care guidance include Livongo, Perry Health, 9am, etc. Given the financial burden that diabetes places on the employer, companies like Virta and Ciba Health are taking a holistic, root-cause approach to type 2 diabetes reversal.

There are also several companies focused on prevention via weight management, nutrition, and care navigation. We are investors in Form Health, whose approach of acquiring patients through physician referrals is a winning strategy. Form’s team of obesity specialists is able to provide more personalized treatment plans and convenient monitoring than a primary care provider has the capacity to provide.

When The Centers for Medicare & Medicaid Services (CMS) made remote patient monitoring (RPM) solutions reimbursable, several well-funded companies were built around this regulation. However, their revenue potential will be put at risk if CMS makes adjustments to these reimbursement rates or scraps them altogether if they don't yield the promised outcomes. For companies in this field to prevail, they will need to be extremely ROI driven and show they can improve management of diabetes through better data, patient experience, and digital programs.

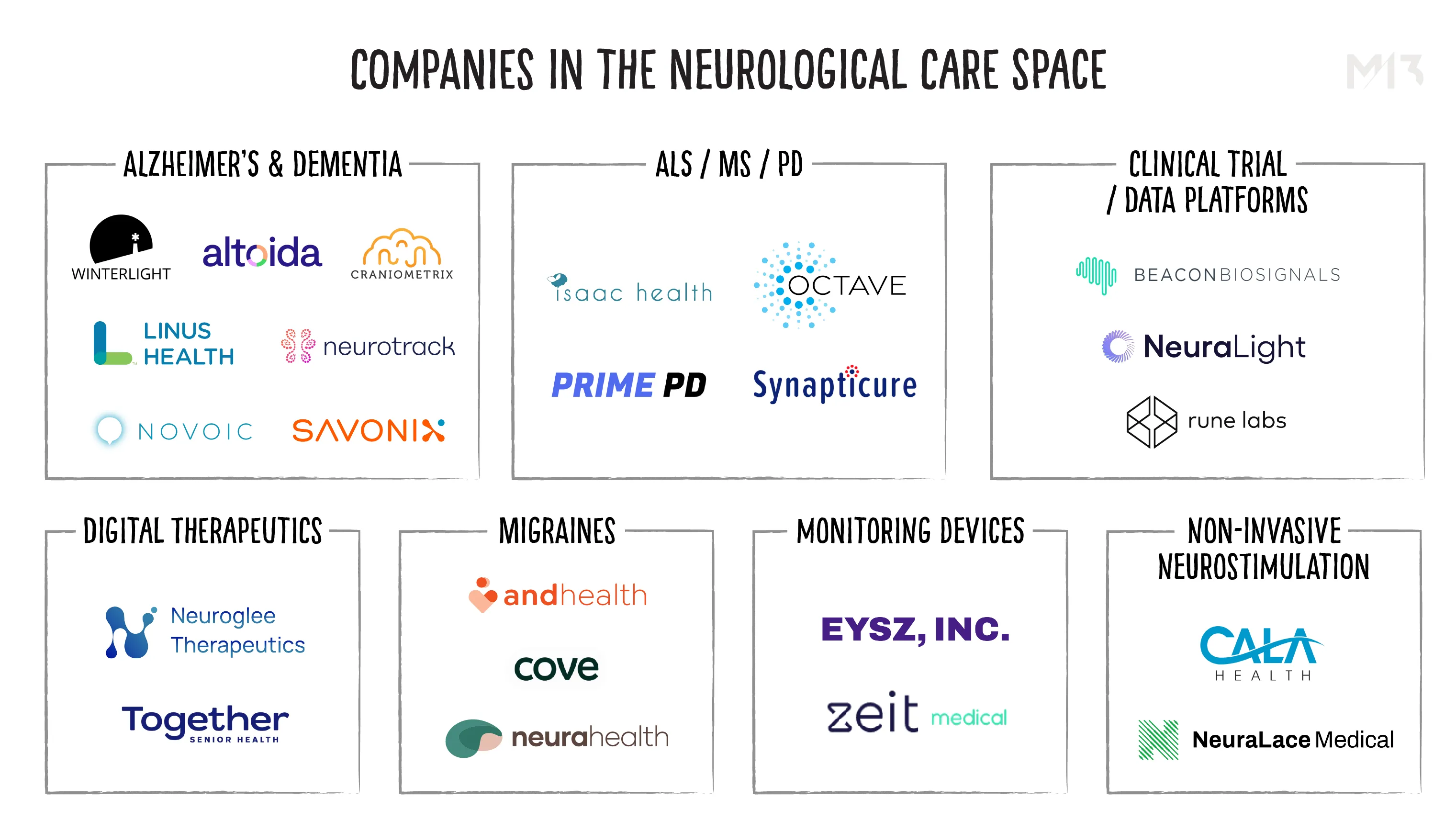

Neurological conditions: detecting early and treating preventatively

Neurology includes a range of conditions. Some of these conditions follow a similar pattern as the other chronic conditions discussed so far: early detection and better disease management can greatly impact patient outcomes.

Today neurological assessments (most commonly for Alzheimer’s and dementia) are infrequent and subjective, usually requiring a doctor's visit. Early detection of neurological conditions is possible with innovations in diagnosis solutions that use wearable data or sensor data from devices. Companies like Savonix and Craniometrix have designed a series of mobile tasks to test for symptoms of dementia, and companies like Winterlight Labs detect cognitive impairment solely with speech analysis. These digital tests can monitor disease progression on a regular basis for those predisposed to Alzheimer’s. Early diagnosis allows a care management team to initiate preventative treatment or make modifications to behavioral factors that can delay or even stop the onset of more severe symptoms.

For other neurological diseases like migraines, companies such as Neura Health can track episodes and identify certain triggers, and the care team is able to suggest personalized lifestyle changes and medication to minimize migraine attacks.

Musculoskeletal (MSK) conditions: virtual-first therapy and optimizing navigation

Our mostly sedentary lifestyle and obesity have given rise to musculoskeletal conditions such as arthritis and back pain. It is one of the largest spend buckets in US healthcare, especially amongst self-funded employers, for whom MSK is typically 17% of healthcare budgets. These conditions can also be managed with medication and physical therapy; if unmanaged, MSK can lead to costly surgeries and procedures and chronic pain.

A number of highly valued digital health companies are emerging in MSK: companies like Hinge Health, Sword Health, and Omada are aiming to use virtual physical therapy and personalized care plans to reduce MSK spend for employers. In order to reduce this spend, virtual MSK platforms must engage patients before they see an MSK specialist which puts them in direct competition with traditional providers. Icon Health has taken the approach of using outcome data, cost data, and expert clinical knowledge to better navigate employees through their unique MSK journey by directing them to the most appropriate provider (in-person or virtual).

Most of the solutions in the MSK market today are sold to employers and are focused on reducing the need for surgery. However, there are far fewer solutions working to empower people to receive the best care and surgical outcomes possible when surgery is the correct approach. It will be interesting to see if Medicare or Medicaid solutions emerge to serve different population groups.

What success in digital care innovation looks like

Successful chronic care solutions often work hand in hand with in-person primary care and specialty doctors, resulting in continuous disease management support for the patient. One of the reasons we invested in Form Health and Agora Health is because they work in collaboration with primary doctors and gastroenterologists respectively, enabling them to better take care of their patients. That they’re leveraging digital solutions to improve patient care further drives efficiencies. It is important that these virtual efficiencies do not come at the expense of holistic patient care, which is why we are supportive of care models that work in conjunction with in-person care teams.

If digital care companies can prove this return on investment and become reimbursable through payers, they can expand their acquisition channels and customer base. Reimbursement is especially critical for chronic care where a cash pay/out-of-pocket only model becomes cost-prohibitive for patients. Credibly proving ROI is a critical but challenging key to success, and, of course, much of this reimbursement is beholden to the new CMS codes.

After an incredibly difficult three years, our nation’s healthcare challenges are only getting worse. Ultimately success looks like improved health for more Americans, and the cost-effective way to achieve that is through patient-centered solutions with a greater focus on education and preventive health. Digital care plays an accessible and affordable role in accelerating early detection, improving habits and lifestyle changes, and ensuring medication management and therapy. We are excited to watch and learn as digital health solutions mature and prove the ROI of virtual solutions.

We at M13 continue to spend more time and deploy capital into digital health companies. If you are building, investing, writing about, or just curious about the space, we hope you’ll join us on the journey.

How to get in touch

We at M13 continue to spend more time and deploy capital into digital health companies. If you are building, investing, writing about, or just curious about the specialty care space, we hope you’ll join us on the journey.

Contact Morgan at morgan@m13.co, and follow her on Twitter at @morgan_blumberg

The views expressed here are those of the individual M13 personnel quoted and are not the views of M13 Holdings Company, LLC (“M13”) or its affiliates. This content is for general informational purposes only and does not and is not intended to constitute legal, business, investment, tax or other advice. You should consult your own advisers as to those matters and should not act or refrain from acting on the basis of this content. This content is not directed to any investors or potential investors, is not an offer or solicitation and may not be used or relied upon in connection with any offer or solicitation with respect to any current or future M13 investment partnership. Past performance is not indicative of future results. Unless otherwise noted, this content is intended to be current only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in funds managed by M13, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by M13 is available at m13.co/portfolio.

At a glance

There are no Cinderella stories. Blockbuster venture successes are always preceded by years of sleepless nights.”

There are no Cinderella stories. Blockbuster venture successes are always preceded by years of sleepless nights.”

—Sarah Tomolonius, M13 Partner & Head of Investor Relations

© 2026 M13. All rights reserved.